Global GDP has grown massively over the last 50 years, but not all countries experienced this economic growth equally.

In 1970, the world’s nominal GDP was just $3.4 trillion. Fast forward a few decades and it had reached $85.3 trillion by 2020. And thanks to shifting dynamics, such as industrialization and the rise and fall of political regimes, the world’s largest economies driving this global growth have changed over time.

As Visual Capitalist's Jenna Ross details in the slides below, using graphics from Ruben Berge Mathisen, show the distribution of global GDP among countries in 1970, 1995, and 2020.

Methodology

Using data from the United Nations, Mathisen collected nominal GDP in U.S. dollars for each country. He then determined each country’s GDP as a share of global GDP and sized each graphic’s bubbles accordingly.

The bubbles were placed according to country latitude and longitude coordinates, but Mathisen programmed the bubbles so that they wouldn’t overlap with each other. For this reason, some countries are slightly displaced from their exact locations on a map.

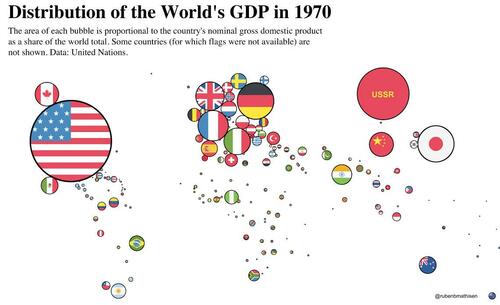

1970: USSR as a Major Player

In 1970, the U.S. accounted for the largest share of global GDP, making up nearly one-third of the world economy. The table below shows the top 10 economies in 1970.

Then a global superpower, the former Union of Soviet Socialist Republics (USSR) came in second place on the list of the world’s largest economies.

In the years leading up to 1970, the USSR had seen impressive GDP growth largely due to adopting Western technologies that increased productivity. However, the USSR’s economy began to stagnate in the ‘70s, and eventually collapsed in 1991.

On the other side, Germany (including both West and East Germany) was the third-largest economy in 1970 after rising from economic ruin following World War II. West Germany’s “Economic Miracle” is largely credited to the introduction of a new currency to replace the Riechsmark, large tax cuts brought in to spur investment, and the removal of price controls.

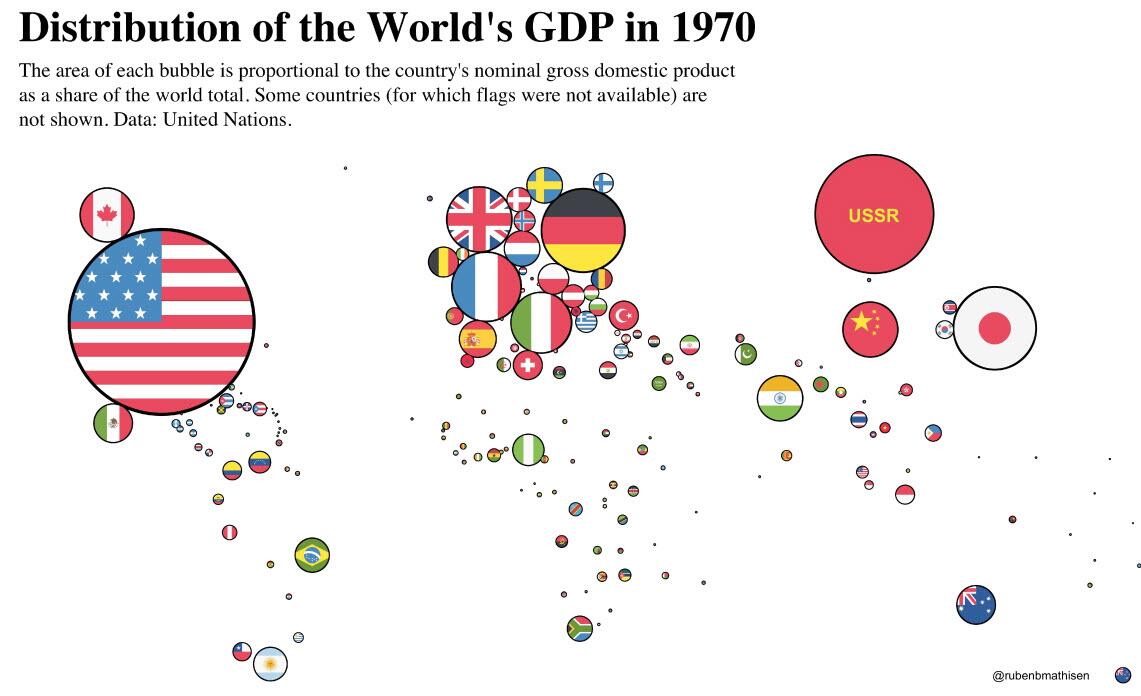

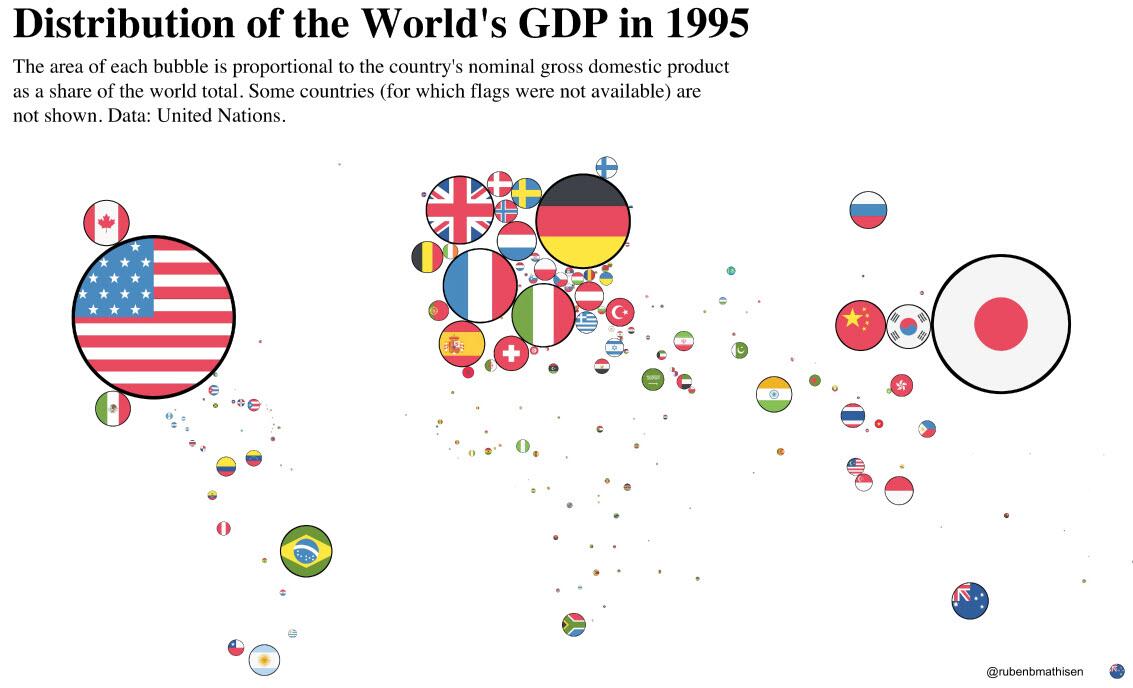

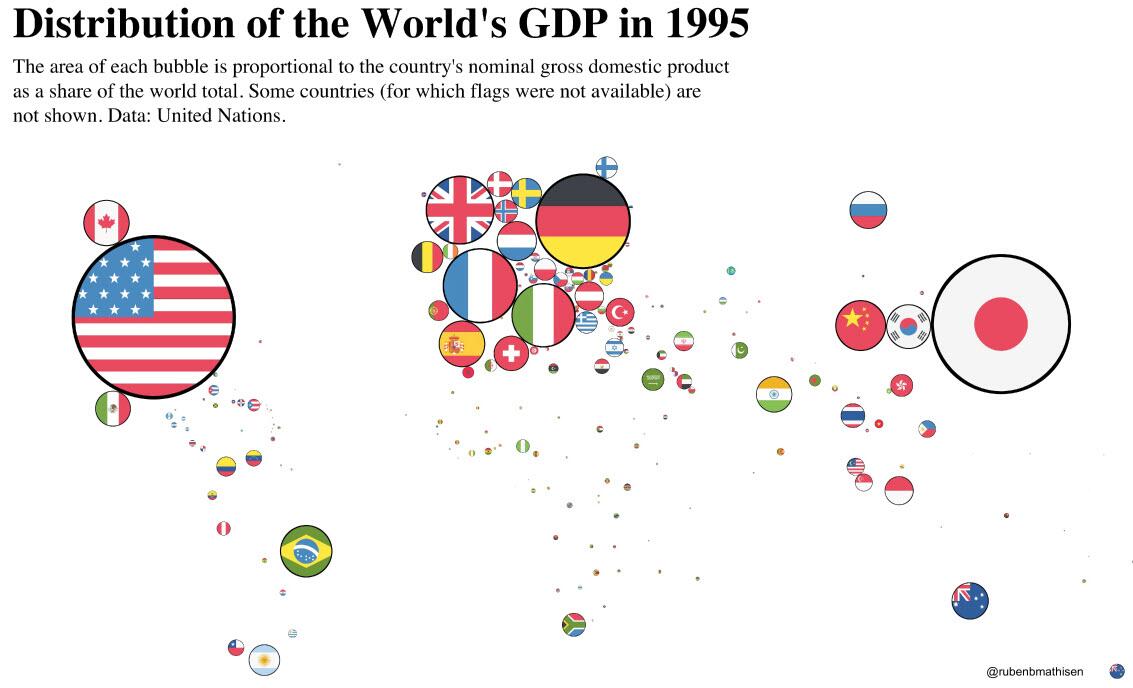

1995: Japan Begins to Slow Down

By 1995, the U.S. still held the top spot on the world’s largest economies list, but the country’s share of global GDP had shrunk.

Meanwhile, Japan had leapfrogged into second place and nearly tripled its share of the global economy compared to 1970. A number of factors played into Japan’s economic success:

-

Large business groups known as keiretsu used their connections to undercut rivals

-

Fierce competition between companies encouraged innovation

-

Tax breaks and cheap credit stimulated investment

-

The well-educated workforce was willing to work extremely long hours

But around 1990, the country’s economy had actually begun to slow down. Japan’s decreasing labor force participation rate and diminishing returns from higher education both could have played a role.

2020: The World’s Largest Economies Shift Again

In 2020, the United States continued to hold onto the number one spot among the world’s largest economies. However, Japan’s slowdown created a rare opportunity for a new powerhouse to emerge: China.

China’s economy saw incredible growth following economic reforms in 1978. The reforms encouraged the formation of private businesses, liberalized foreign trade and investment, relaxed state control over some prices, and invested in industrial production and the education of its workforce. With profit incentives introduced to private businesses, productivity increased.

China was also positioned as a cheap manufacturing hub for multinational corporations. Since rising into contention, the country has become the world’s largest exporter.

India held the title of the sixth largest economy in 2020. Similar to China, the country’s growth came from relaxed economic restrictions, and it has seen particularly strong growth within the service sector, including telecommunications, IT, and software.

With dynamics shifting, which countries will be on the leaderboard in another 25 years?

Global GDP has grown massively over the last 50 years, but not all countries experienced this economic growth equally.

In 1970, the world’s nominal GDP was just $3.4 trillion. Fast forward a few decades and it had reached $85.3 trillion by 2020. And thanks to shifting dynamics, such as industrialization and the rise and fall of political regimes, the world’s largest economies driving this global growth have changed over time.

As Visual Capitalist’s Jenna Ross details in the slides below, using graphics from Ruben Berge Mathisen, show the distribution of global GDP among countries in 1970, 1995, and 2020.

Methodology

Using data from the United Nations, Mathisen collected nominal GDP in U.S. dollars for each country. He then determined each country’s GDP as a share of global GDP and sized each graphic’s bubbles accordingly.

The bubbles were placed according to country latitude and longitude coordinates, but Mathisen programmed the bubbles so that they wouldn’t overlap with each other. For this reason, some countries are slightly displaced from their exact locations on a map.

1970: USSR as a Major Player

In 1970, the U.S. accounted for the largest share of global GDP, making up nearly one-third of the world economy. The table below shows the top 10 economies in 1970.

Then a global superpower, the former Union of Soviet Socialist Republics (USSR) came in second place on the list of the world’s largest economies.

In the years leading up to 1970, the USSR had seen impressive GDP growth largely due to adopting Western technologies that increased productivity. However, the USSR’s economy began to stagnate in the ‘70s, and eventually collapsed in 1991.

On the other side, Germany (including both West and East Germany) was the third-largest economy in 1970 after rising from economic ruin following World War II. West Germany’s “Economic Miracle” is largely credited to the introduction of a new currency to replace the Riechsmark, large tax cuts brought in to spur investment, and the removal of price controls.

1995: Japan Begins to Slow Down

By 1995, the U.S. still held the top spot on the world’s largest economies list, but the country’s share of global GDP had shrunk.

Meanwhile, Japan had leapfrogged into second place and nearly tripled its share of the global economy compared to 1970. A number of factors played into Japan’s economic success:

-

Large business groups known as keiretsu used their connections to undercut rivals

-

Fierce competition between companies encouraged innovation

-

Tax breaks and cheap credit stimulated investment

-

The well-educated workforce was willing to work extremely long hours

But around 1990, the country’s economy had actually begun to slow down. Japan’s decreasing labor force participation rate and diminishing returns from higher education both could have played a role.

2020: The World’s Largest Economies Shift Again

In 2020, the United States continued to hold onto the number one spot among the world’s largest economies. However, Japan’s slowdown created a rare opportunity for a new powerhouse to emerge: China.

China’s economy saw incredible growth following economic reforms in 1978. The reforms encouraged the formation of private businesses, liberalized foreign trade and investment, relaxed state control over some prices, and invested in industrial production and the education of its workforce. With profit incentives introduced to private businesses, productivity increased.

China was also positioned as a cheap manufacturing hub for multinational corporations. Since rising into contention, the country has become the world’s largest exporter.

India held the title of the sixth largest economy in 2020. Similar to China, the country’s growth came from relaxed economic restrictions, and it has seen particularly strong growth within the service sector, including telecommunications, IT, and software.

With dynamics shifting, which countries will be on the leaderboard in another 25 years?