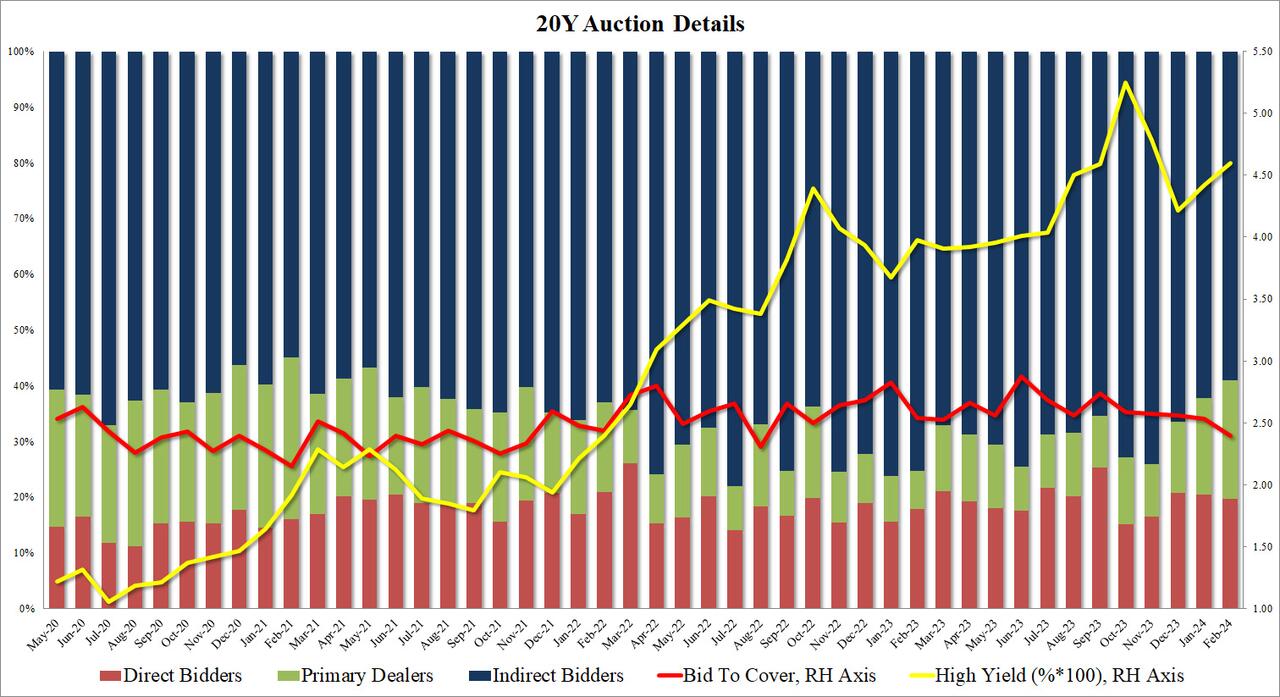

Despite some optimistic expectations (most notably from Bloomberg's Markets Live blog) that today's 20Y auction would "stop through with long list of positives", moments ago the Treasury sold 20Y paper with disastrous metrics which sent yields sharply higher across the board.

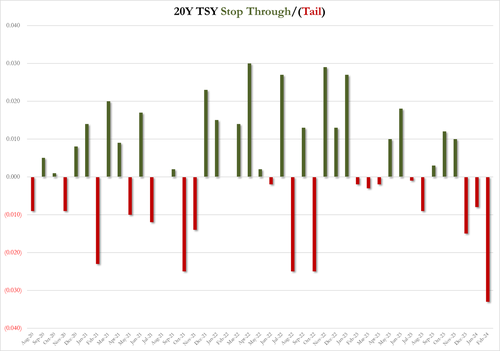

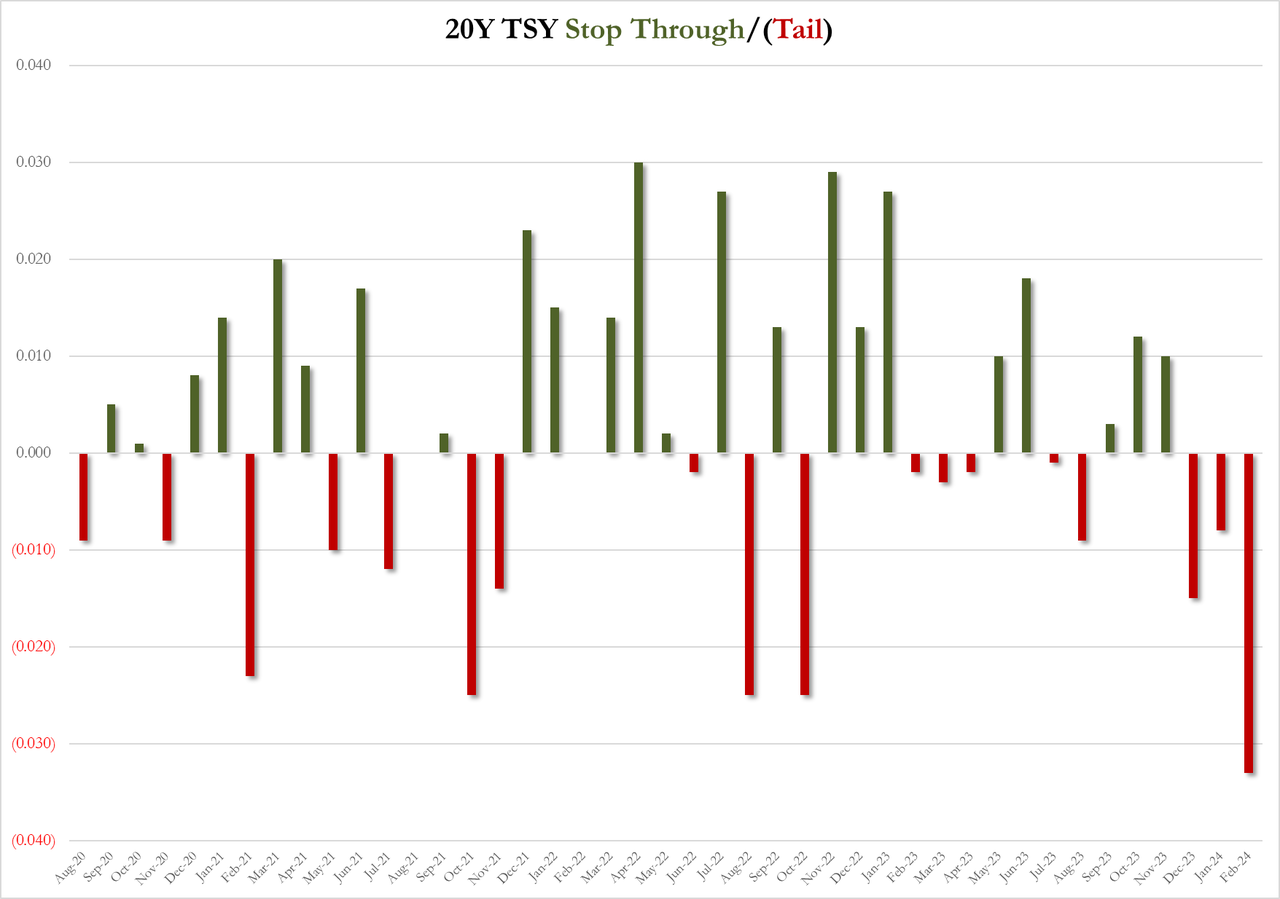

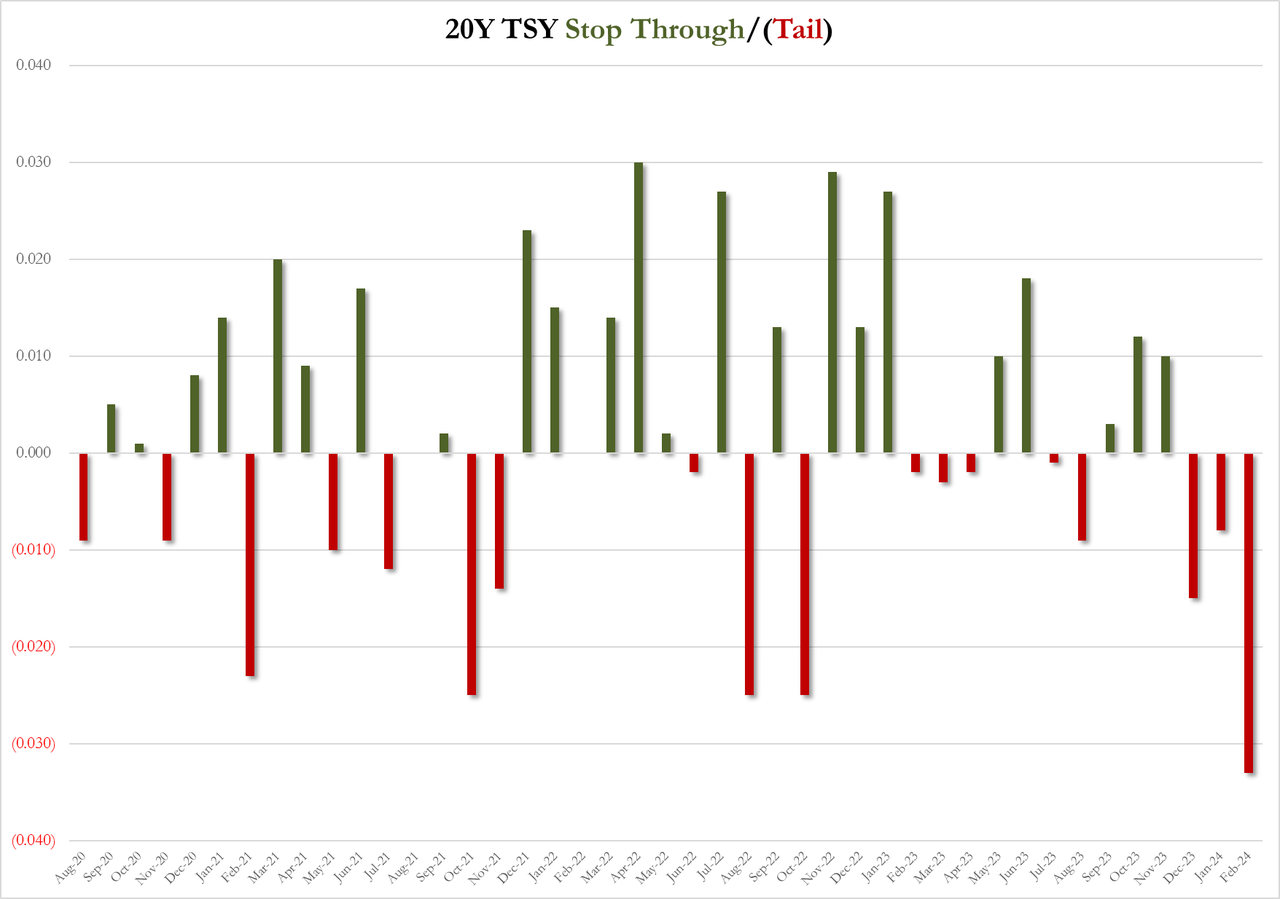

The high yield of 4.595% was well above last month's 4.423% but worse, it tailed the When Issued 4.562% by a whopping 3.30bps, which was the biggest tail on record for the tenor since the 20Y auction was introduced in May 2020.

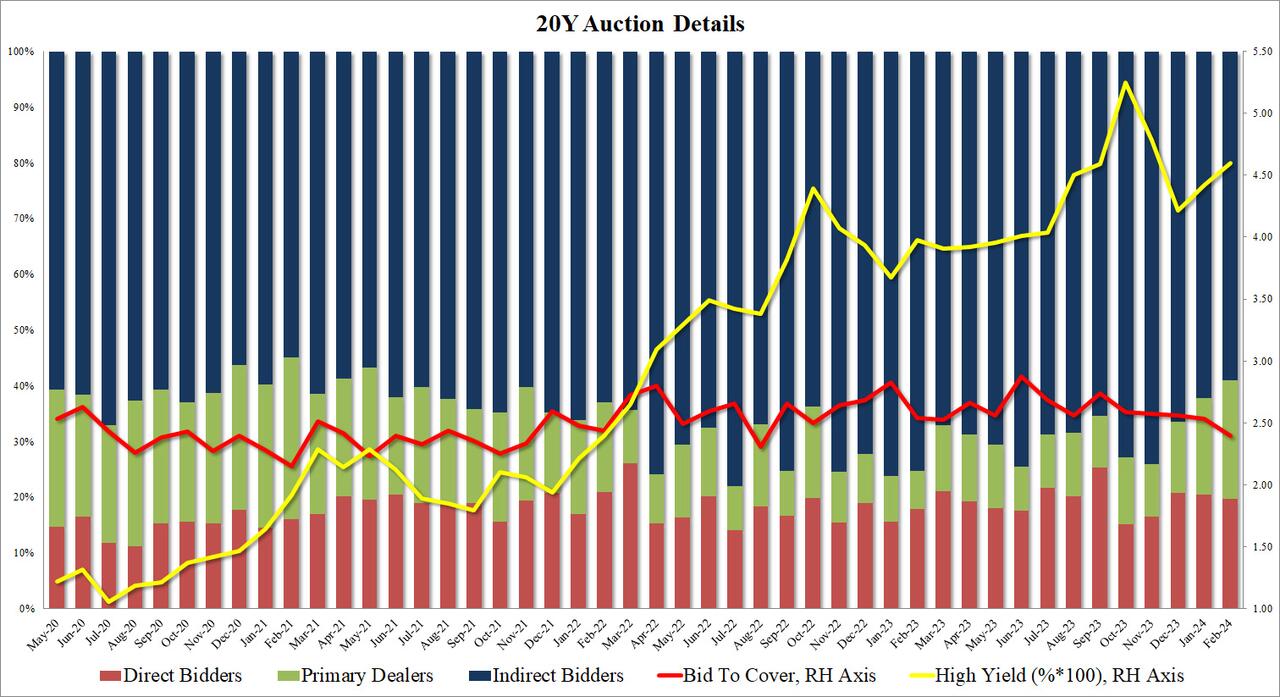

The bid to cover tumbled to 2.39, down from 2.53, well below the 2.59 six-auction average, and was the lowest since August 2022.

The internals were even uglier, with Indirects awarded just 59.08%, lower than last month's 62.16%, sharply lower than recent average of 68.2% and the lowest since May 2021. And with Directs taking down 19.7%, Dealers were left holding 21.2%, the most since May 2021.

Overall this was a very ugly auction, despite the substantial concession thanks to the ongoing selling in rates (perhaps due to the $13.5BN in debt issuance just announced by Cisco to fund its Splunk purchase), and while it is unclear why demand was so terrible perhaps one can attribute it to nerves from today's FOMC Minutes which however should be a non-event as they are already rather dated and do not reflect the latest reflationary spike.

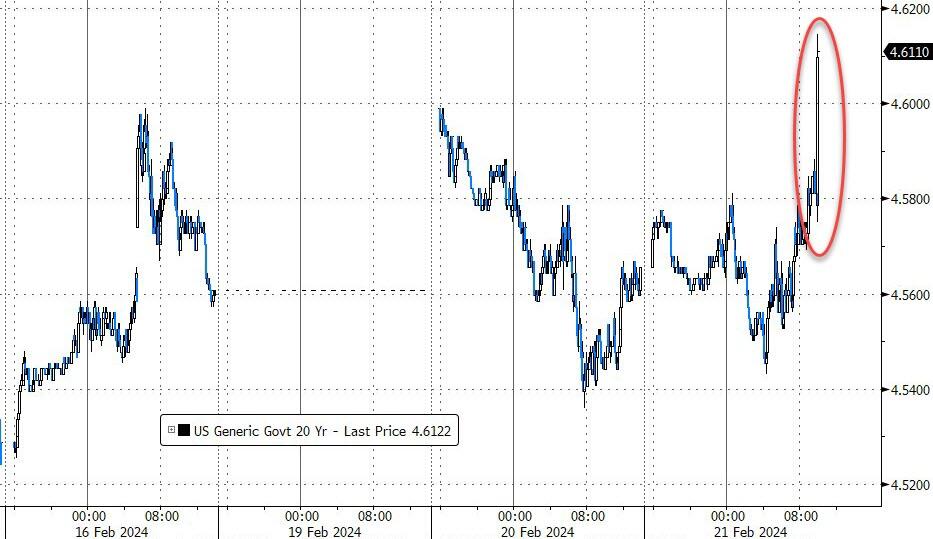

In any case, yields promptly spiked with the 10Y rising as high as 4.325% before retracing some of the move, which also sent stocks sliding briefly before recovering.

Despite some optimistic expectations (most notably from Bloomberg’s Markets Live blog) that today’s 20Y auction would “stop through with long list of positives”, moments ago the Treasury sold 20Y paper with disastrous metrics which sent yields sharply higher across the board.

The high yield of 4.595% was well above last month’s 4.423% but worse, it tailed the When Issued 4.562% by a whopping 3.30bps, which was the biggest tail on record for the tenor since the 20Y auction was introduced in May 2020.

The bid to cover tumbled to 2.39, down from 2.53, well below the 2.59 six-auction average, and was the lowest since August 2022.

The internals were even uglier, with Indirects awarded just 59.08%, lower than last month’s 62.16%, sharply lower than recent average of 68.2% and the lowest since May 2021. And with Directs taking down 19.7%, Dealers were left holding 21.2%, the most since May 2021.

Overall this was a very ugly auction, despite the substantial concession thanks to the ongoing selling in rates (perhaps due to the $13.5BN in debt issuance just announced by Cisco to fund its Splunk purchase), and while it is unclear why demand was so terrible perhaps one can attribute it to nerves from today’s FOMC Minutes which however should be a non-event as they are already rather dated and do not reflect the latest reflationary spike.

In any case, yields promptly spiked with the 10Y rising as high as 4.325% before retracing some of the move, which also sent stocks sliding briefly before recovering.

Loading…