With everyone obsessing over UK lettuce and the Fed blowing up the US economy, there was not enough digital ink to discuss the supreme irony of Biden unleashing another release of oil from the Midterm Petroleum Reserve and... oil surging.

Unfortunately for the ever more addled president, this is just the start.

On Wednesday, Amrita Sen, co-founder and research director at consultants Energy Aspects, said on Bloomberg TV that the market risks losing Russian barrels in December as EU restrictions on imports and shipping potentially dissuade tanker owners from moving that country’s crude.

As a result, oil prices “are going to be headed well over $100” going into December while near-term prices are pressured by strikes in France and lockdowns in China that suppress demand. However, once those wear off, Europe will have to stop importing 1m to 1.5m b/d of Russian crude when embargo on seaborne shipments takes effect in December; those barrels - as Zoltan Pozsar explained all the way back in March and April - will have to be shipped to more distant markets with transport times of 30-50 days vs only 3-4 days to Europe, causing surging costs and substantial delays.

Separately, if shipowners decide that the risk of sanctions is too high to move Russian crude “you will lose some shipping and that will tie up more oil.”

This reminds us of something Goldman flow trader Rich Privorotsky wrote in this morning's market wrap (available to pro subs), when we cautioned that hs is "getting increasingly concerned about oil market supply beyond the midterms. This proposal from the EU is not helping my anxiety as the proposed oil cap could have some pretty major consequences in the shipping market" Here's why as Bloomberg noted earlier:

“In the event that a vessel under the flag of a third country has transported Russian crude oil or petroleum products purchased at a price above the price cap, it should be prohibited to provide technical assistance, brokering services, financing or financial assistance, including insurance, related to any transport in the future by that vessel of crude oil or petroleum products”

That will certainly spark a profound chilling effect across the entire industry.

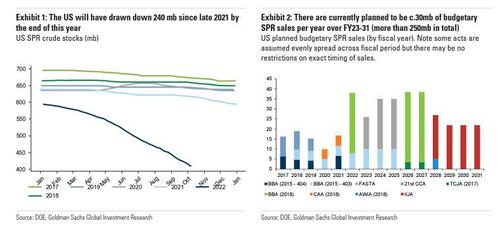

But what about Biden's SPR drain - is it really that useless, and won't it help at least a little? Well, according to Sen, limits on how low stocks can be drawn mean sales won’t be as large as some expect (analysts are expecting a release of as much as 100m bbl; with 26m bbl to be released between December and February).

But the clearest explanation why Biden's last-ditch SPR release won't do jack, comes from Goldman's commodity strategists led by Jeff Currie who published a note late on Thursday (and also available to pro subs), in which they write the following:

Following OPEC+’s surprise 2mb/d cut on October 5, the Biden administration was quick to imply a policy response, concerned about rising gasoline prices fact sheet into November 8 midterms. On October 18, the White House released an energy policy . The speech highlights various ahead of President Biden’s speech concerns and actions taken by the administration to “strengthen energy security, encourage production, and bring down costs.

The 15 mb SPR drawdown (the final tranche of the 180 mb Spring announcement) drew headlines, but of more interest was the plans to refill the SPR at fixed prices for future delivery “at or below about $67-72/bbl”, offering some support to crude prices below the ‘shale band’. This truncation of the price distribution should encourage investment in growing production - if only marginally. We find marketing and refining margins in the US to be elevated, but the latter is a function of exorbitant international energy prices as well as structurally tight refining markets.

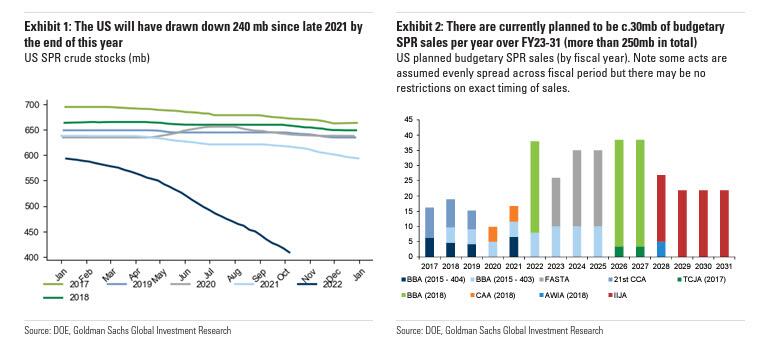

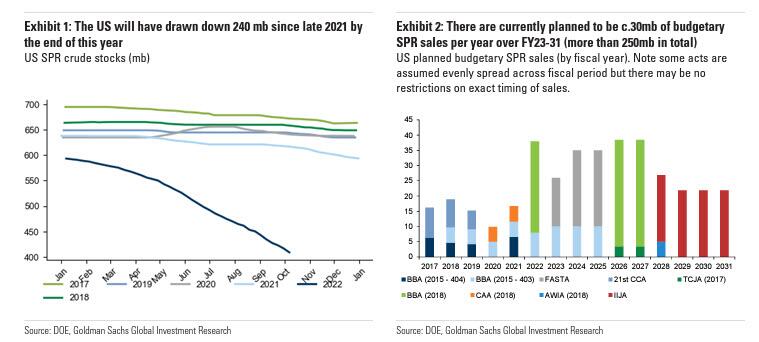

Additional headlines since the OPEC+ meeting have highlighted other policy options available to the Administration. We find incremental SPR sales as the most likely action (16mb is available from FY2023 Congressionally mandated sales), although this remains price dependent: requiring higher prices than present, and likely closer to $125/bbl following the midterms. Such a release is likely to have only a modest influence (<$5/bbl) on oil prices however.

All options have trade-offs. Product export bans in particular could send wholesale global distillate/gasoline prices up $150/$50/bbl respectively (to $300/150/bbl) and still risk shortages and higher prices domestically - especially in coastal regions. All responses leave the ultimate cause of energy underinvestment unaddressed.

We continue to expect headlines into next month’s midterm elections as the US administration attempts to exert downward pressure on retail prices. However, we think action at current price levels remains unlikely. This policy reflexivity is reflected in our current forecasts ($115/bbl Brent in 1Q23 ), as the deficits we expect, following OPEC+’s decision to cut, look unsustainably bullish given scarce inventories and our balance outlook. The risk of inventory depletion and price spikes requiring demand destruction as a rebalancing of last resort could yet move prices $30+/bbl higher.

There is more in the full Goldman reports, including an analysis on why a product export ban will exacerbated the global shortage of refining capacity, why a gasoline federal tax holiday would be modest in impact, why easing sanctions on Venezuela is not a quick fix, and why the “NOPEC” bill has only very limited upside.

For once, we completely agree with Goldman. More in the full note available to pro subs.

With everyone obsessing over UK lettuce and the Fed blowing up the US economy, there was not enough digital ink to discuss the supreme irony of Biden unleashing another release of oil from the Midterm Petroleum Reserve and… oil surging.

Unfortunately for the ever more addled president, this is just the start.

On Wednesday, Amrita Sen, co-founder and research director at consultants Energy Aspects, said on Bloomberg TV that the market risks losing Russian barrels in December as EU restrictions on imports and shipping potentially dissuade tanker owners from moving that country’s crude.

As a result, oil prices “are going to be headed well over $100” going into December while near-term prices are pressured by strikes in France and lockdowns in China that suppress demand. However, once those wear off, Europe will have to stop importing 1m to 1.5m b/d of Russian crude when embargo on seaborne shipments takes effect in December; those barrels – as Zoltan Pozsar explained all the way back in March and April – will have to be shipped to more distant markets with transport times of 30-50 days vs only 3-4 days to Europe, causing surging costs and substantial delays.

Separately, if shipowners decide that the risk of sanctions is too high to move Russian crude “you will lose some shipping and that will tie up more oil.”

This reminds us of something Goldman flow trader Rich Privorotsky wrote in this morning’s market wrap (available to pro subs), when we cautioned that hs is “getting increasingly concerned about oil market supply beyond the midterms. This proposal from the EU is not helping my anxiety as the proposed oil cap could have some pretty major consequences in the shipping market” Here’s why as Bloomberg noted earlier:

“In the event that a vessel under the flag of a third country has transported Russian crude oil or petroleum products purchased at a price above the price cap, it should be prohibited to provide technical assistance, brokering services, financing or financial assistance, including insurance, related to any transport in the future by that vessel of crude oil or petroleum products”

That will certainly spark a profound chilling effect across the entire industry.

But what about Biden’s SPR drain – is it really that useless, and won’t it help at least a little? Well, according to Sen, limits on how low stocks can be drawn mean sales won’t be as large as some expect (analysts are expecting a release of as much as 100m bbl; with 26m bbl to be released between December and February).

But the clearest explanation why Biden’s last-ditch SPR release won’t do jack, comes from Goldman’s commodity strategists led by Jeff Currie who published a note late on Thursday (and also available to pro subs), in which they write the following:

Following OPEC+’s surprise 2mb/d cut on October 5, the Biden administration was quick to imply a policy response, concerned about rising gasoline prices fact sheet into November 8 midterms. On October 18, the White House released an energy policy . The speech highlights various ahead of President Biden’s speech concerns and actions taken by the administration to “strengthen energy security, encourage production, and bring down costs.

The 15 mb SPR drawdown (the final tranche of the 180 mb Spring announcement) drew headlines, but of more interest was the plans to refill the SPR at fixed prices for future delivery “at or below about $67-72/bbl”, offering some support to crude prices below the ‘shale band’. This truncation of the price distribution should encourage investment in growing production – if only marginally. We find marketing and refining margins in the US to be elevated, but the latter is a function of exorbitant international energy prices as well as structurally tight refining markets.

Additional headlines since the OPEC+ meeting have highlighted other policy options available to the Administration. We find incremental SPR sales as the most likely action (16mb is available from FY2023 Congressionally mandated sales), although this remains price dependent: requiring higher prices than present, and likely closer to $125/bbl following the midterms. Such a release is likely to have only a modest influence (<$5/bbl) on oil prices however.

All options have trade-offs. Product export bans in particular could send wholesale global distillate/gasoline prices up $150/$50/bbl respectively (to $300/150/bbl) and still risk shortages and higher prices domestically – especially in coastal regions. All responses leave the ultimate cause of energy underinvestment unaddressed.

We continue to expect headlines into next month’s midterm elections as the US administration attempts to exert downward pressure on retail prices. However, we think action at current price levels remains unlikely. This policy reflexivity is reflected in our current forecasts ($115/bbl Brent in 1Q23 ), as the deficits we expect, following OPEC+’s decision to cut, look unsustainably bullish given scarce inventories and our balance outlook. The risk of inventory depletion and price spikes requiring demand destruction as a rebalancing of last resort could yet move prices $30+/bbl higher.

There is more in the full Goldman reports, including an analysis on why a product export ban will exacerbated the global shortage of refining capacity, why a gasoline federal tax holiday would be modest in impact, why easing sanctions on Venezuela is not a quick fix, and why the “NOPEC” bill has only very limited upside.

For once, we completely agree with Goldman. More in the full note available to pro subs.