With just 12 hours to go until Nancy Pelosi is reportedly scheduled to land in Taiwan (around 10:20pm local time on Tuesday), prevailing consensus is that for all the posturing and heated rhetoric, nothing much will happen. Consider the following quote from General Frank Kearny:

"The Chinese have stated that they would attempt to deter her flight using Chinese aircraft creating a threatening situation which could escalate. I seriously doubt they would shoot it down as also threatened. I suspect the Taiwanese would be threatened as well with provocative demonstrations of air and naval actions. I don’t believe these are just threats. I believe some action will occur with the potential for unintended consequences.”

Or the following assessment from General Spider Marks:

“China will be diplomatically aggressive...tough talk, little likelihood China will militarily interfere with Pelosi’s visit should she get the green light from President Biden to go. China, not unlike the Russians and Iranians in the Persian Gulf, may threaten Pelosi’s aircraft or possibly US naval ships which are underway in the vicinity. The risks are too high for the Chinese to interfere and not expect (and wargame) the worse possible outcome.”

And while we certainly hope that such sanguine assessments are accurate considering that the alternative is global thermonuclear war, many are forgetting that while the reeling Biden administration would certainly benefit from the distraction that is a limited military conflict, so would China. The reason for that is that war may not be good for a whole lot of things, when it comes to economic growth it is the proverbial Keynesian jackpot.

And China certainly needs economic growth. Moments ago Bloomberg blasted out a flashing red headlines saying that...

- *CHINESE LEADERS SAY GDP GOAL IS GUIDANCE, NOT A HARD TARGET

In the article, Bloomberg reports that China’s top leaders told government officials last week that this year’s economic growth target of “around 5.5%” should serve as guidance rather than a hard target that must be hit.

Leaders held meetings with ministerial and provincial-level officials last week, during which they were told the target won’t be used to evaluate their performance and there won’t be penalties for failing to achieve it, according to the people, who asked not to be identified because they were not authorized to discuss the matter publicly. The leaders also acknowledged that the chances of meeting the target were slim, the people said.

This is certainly plausible, as there is a very clear reason why China's economy is suddenly sinking rapidly, and it has everything to do with China's biggest asset class: property.

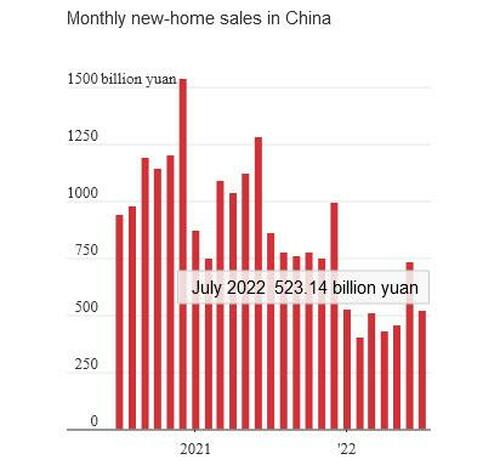

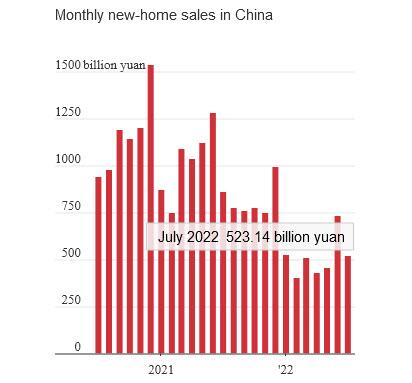

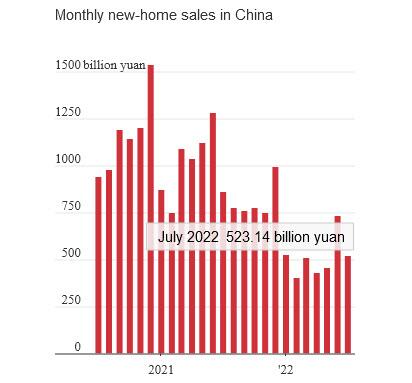

As the WSJ reported on Sunday, a short-lived, 2-month recovery in China’s home sales ended with a bang in July, as the widespread mortgage revolt discussed here previously which erupted over concerns that ailing property developers wouldn’t be able to deliver still-unfinished apartments weighed on demand.

Sales at the country’s top 100 property developers fell 40% in July from the same period last year to the equivalent of $77.6 billion, or 523.14 billion yuan, according to data released Sunday by CRIC, a Chinese real-estate data provider.

But while the annual numbers have been a well-known horrorshow following last year's implosion of Evergrande and most of its property developer peers, July sales were also down 28.6% sequentially from June, ending a two-month recovery in month-to-month sales growth. The silver lining: apartment sales showed increases in May and June from the previous months, as activity picked up following Covid lockdowns in Shanghai and other Chinese cities earlier this year.

Week-over-week data put together earlier by CRIC to study the impact of the mortgage revolt had signaled the July decline. In 30 cities CRIC determined to have been seriously affected by the revolt, new home sales dropped by 12% in the week ended July 10 from the week before, then fell 41% in the week ended July 17.

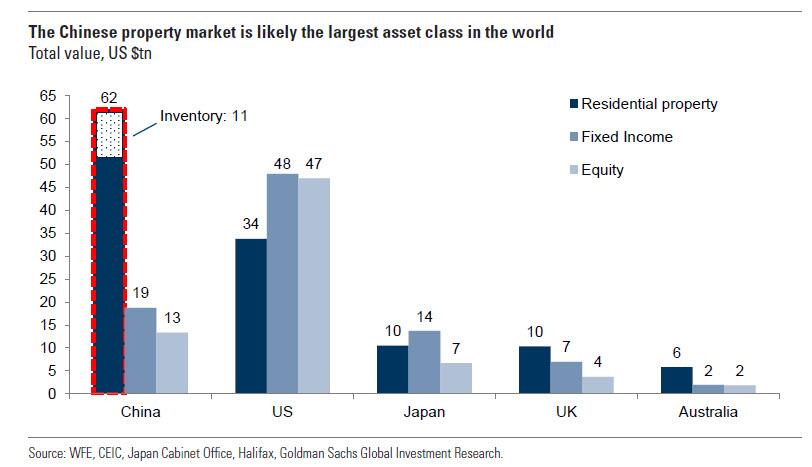

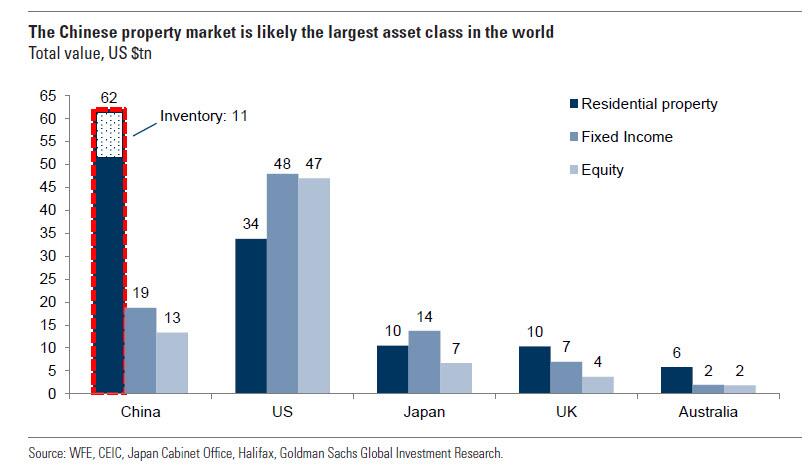

China’s private-sector property developers went on a yearslong, debt-fueled building boom, selling homes before they were built, until a funding crisis that began last year led to defaults and stalled projects. Buyers who typically sank large down payments into those homes have been venting their frustrations all summer. Meanwhile the value of China's property market, which Goldman has estimated at $62 trillion, making it the world's largest standalone asset class....

... is cracking much to the horror of Beijing which knows that if Chinese housing, which is where the bulk of China's middle class has parked its net worth, goes, it may well be game over so might as well spark a foreign conflict as an economic renaissance Hail Mary.

Going back to the immediate cause for the latest plunge in new home sales, the culprit is the mortgage revolt which started at the end of June at an Evergrande project in Jingdezhen, in central China’s Jiangxi province, where frustrated home buyers threatened to renege on mortgages on unfinished properties. Thousands of buyers from roughly 320 projects across the country had followed suit as of July 29, according to a tally of statements from homeowners who said they will stop paying their mortgages circulating on GitHub.

Home buyers -some waving signs saying “Construction stops and mortgage stops!” -say the threat to halt payments is the only way to get their voices heard as projects stall and delivery times drag out.

But the bigger problem is that China's broadly slowing economy - where property has traditionally been one of the core support pillars - is biting into employment and incomes is adding to the pressure. As a result, some buyers say they are increasingly unwilling to keep paying for a home they aren’t sure they will ever receive (in China, one purchases a new home while it is still in production, with little to no assurance one will get a finished product). More home buyers are choosing second-hand homes or new ones built by state-owned developers, which are typically in a stronger financial position.

And so, pressure on the government is building, but hopes for a large real-estate rescue package from Beijing remain unrealized. The Politburo, China’s top policy-making body, made clear recently that local governments are ultimately responsible for fixing the property woes in their markets. At the same time, amid China's austerity, budget-strapped local authorities have strained to boost property demand, resorting to increasingly creative measures. Dozens of cities have lowered down payments and interest rates. Some are offering outright cash subsidies. Others have announced relief funds for cash-strapped developers or plans to take over troubled projects.

“But the sector won’t stabilize if developers’ liquidity crunch is not relieved,” said Song Hongwei, a research director of Tongce Research Institute, which tracks and analyzes China’s real-estate market.

It is in this context that a (limited) war is just the desired catalyst needed to reverse China's accelerating economic contraction. And all that Beijing needed was an appropriate opportunity to launch one... an opportunity which has presented itself thanks to Nancy Pelosi's unprecedented boondoggle into Taiwan which we are confident Beijing will now milk (or rather vodka) for all it's worth.

With just 12 hours to go until Nancy Pelosi is reportedly scheduled to land in Taiwan (around 10:20pm local time on Tuesday), prevailing consensus is that for all the posturing and heated rhetoric, nothing much will happen. Consider the following quote from General Frank Kearny:

“The Chinese have stated that they would attempt to deter her flight using Chinese aircraft creating a threatening situation which could escalate. I seriously doubt they would shoot it down as also threatened. I suspect the Taiwanese would be threatened as well with provocative demonstrations of air and naval actions. I don’t believe these are just threats. I believe some action will occur with the potential for unintended consequences.”

Or the following assessment from General Spider Marks:

“China will be diplomatically aggressive…tough talk, little likelihood China will militarily interfere with Pelosi’s visit should she get the green light from President Biden to go. China, not unlike the Russians and Iranians in the Persian Gulf, may threaten Pelosi’s aircraft or possibly US naval ships which are underway in the vicinity. The risks are too high for the Chinese to interfere and not expect (and wargame) the worse possible outcome.”

And while we certainly hope that such sanguine assessments are accurate considering that the alternative is global thermonuclear war, many are forgetting that while the reeling Biden administration would certainly benefit from the distraction that is a limited military conflict, so would China. The reason for that is that war may not be good for a whole lot of things, when it comes to economic growth it is the proverbial Keynesian jackpot.

And China certainly needs economic growth. Moments ago Bloomberg blasted out a flashing red headlines saying that…

- *CHINESE LEADERS SAY GDP GOAL IS GUIDANCE, NOT A HARD TARGET

In the article, Bloomberg reports that China’s top leaders told government officials last week that this year’s economic growth target of “around 5.5%” should serve as guidance rather than a hard target that must be hit.

Leaders held meetings with ministerial and provincial-level officials last week, during which they were told the target won’t be used to evaluate their performance and there won’t be penalties for failing to achieve it, according to the people, who asked not to be identified because they were not authorized to discuss the matter publicly. The leaders also acknowledged that the chances of meeting the target were slim, the people said.

This is certainly plausible, as there is a very clear reason why China’s economy is suddenly sinking rapidly, and it has everything to do with China’s biggest asset class: property.

As the WSJ reported on Sunday, a short-lived, 2-month recovery in China’s home sales ended with a bang in July, as the widespread mortgage revolt discussed here previously which erupted over concerns that ailing property developers wouldn’t be able to deliver still-unfinished apartments weighed on demand.

Sales at the country’s top 100 property developers fell 40% in July from the same period last year to the equivalent of $77.6 billion, or 523.14 billion yuan, according to data released Sunday by CRIC, a Chinese real-estate data provider.

But while the annual numbers have been a well-known horrorshow following last year’s implosion of Evergrande and most of its property developer peers, July sales were also down 28.6% sequentially from June, ending a two-month recovery in month-to-month sales growth. The silver lining: apartment sales showed increases in May and June from the previous months, as activity picked up following Covid lockdowns in Shanghai and other Chinese cities earlier this year.

Week-over-week data put together earlier by CRIC to study the impact of the mortgage revolt had signaled the July decline. In 30 cities CRIC determined to have been seriously affected by the revolt, new home sales dropped by 12% in the week ended July 10 from the week before, then fell 41% in the week ended July 17.

China’s private-sector property developers went on a yearslong, debt-fueled building boom, selling homes before they were built, until a funding crisis that began last year led to defaults and stalled projects. Buyers who typically sank large down payments into those homes have been venting their frustrations all summer. Meanwhile the value of China’s property market, which Goldman has estimated at $62 trillion, making it the world’s largest standalone asset class….

… is cracking much to the horror of Beijing which knows that if Chinese housing, which is where the bulk of China’s middle class has parked its net worth, goes, it may well be game over so might as well spark a foreign conflict as an economic renaissance Hail Mary.

Going back to the immediate cause for the latest plunge in new home sales, the culprit is the mortgage revolt which started at the end of June at an Evergrande project in Jingdezhen, in central China’s Jiangxi province, where frustrated home buyers threatened to renege on mortgages on unfinished properties. Thousands of buyers from roughly 320 projects across the country had followed suit as of July 29, according to a tally of statements from homeowners who said they will stop paying their mortgages circulating on GitHub.

Home buyers -some waving signs saying “Construction stops and mortgage stops!” -say the threat to halt payments is the only way to get their voices heard as projects stall and delivery times drag out.

But the bigger problem is that China’s broadly slowing economy – where property has traditionally been one of the core support pillars – is biting into employment and incomes is adding to the pressure. As a result, some buyers say they are increasingly unwilling to keep paying for a home they aren’t sure they will ever receive (in China, one purchases a new home while it is still in production, with little to no assurance one will get a finished product). More home buyers are choosing second-hand homes or new ones built by state-owned developers, which are typically in a stronger financial position.

And so, pressure on the government is building, but hopes for a large real-estate rescue package from Beijing remain unrealized. The Politburo, China’s top policy-making body, made clear recently that local governments are ultimately responsible for fixing the property woes in their markets. At the same time, amid China’s austerity, budget-strapped local authorities have strained to boost property demand, resorting to increasingly creative measures. Dozens of cities have lowered down payments and interest rates. Some are offering outright cash subsidies. Others have announced relief funds for cash-strapped developers or plans to take over troubled projects.

“But the sector won’t stabilize if developers’ liquidity crunch is not relieved,” said Song Hongwei, a research director of Tongce Research Institute, which tracks and analyzes China’s real-estate market.

It is in this context that a (limited) war is just the desired catalyst needed to reverse China’s accelerating economic contraction. And all that Beijing needed was an appropriate opportunity to launch one… an opportunity which has presented itself thanks to Nancy Pelosi’s unprecedented boondoggle into Taiwan which we are confident Beijing will now milk (or rather vodka) for all it’s worth.