Authored by Michael Lebowitz via RealInvestementAdvice.com,

On Sunday, March 16, 2008, Bear Stearns was bought by JPM, with support and financial guarantees from the Fed, for $2 a share. It was quite the fall from $170 a year earlier.

Wall Street was in the early rounds of a bout with unprecedented financial instability, and the economy would soon follow. Investors were relieved Bear Stearns avoided bankruptcy in spite of the ominous clouds on the horizon and recent financial instability. Within hours of the market opening following the Bear Stearns takeover, stocks started rising and didn’t look back for a month.

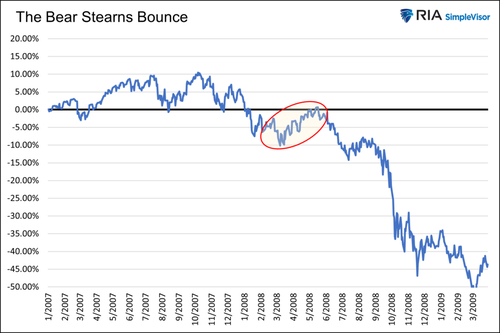

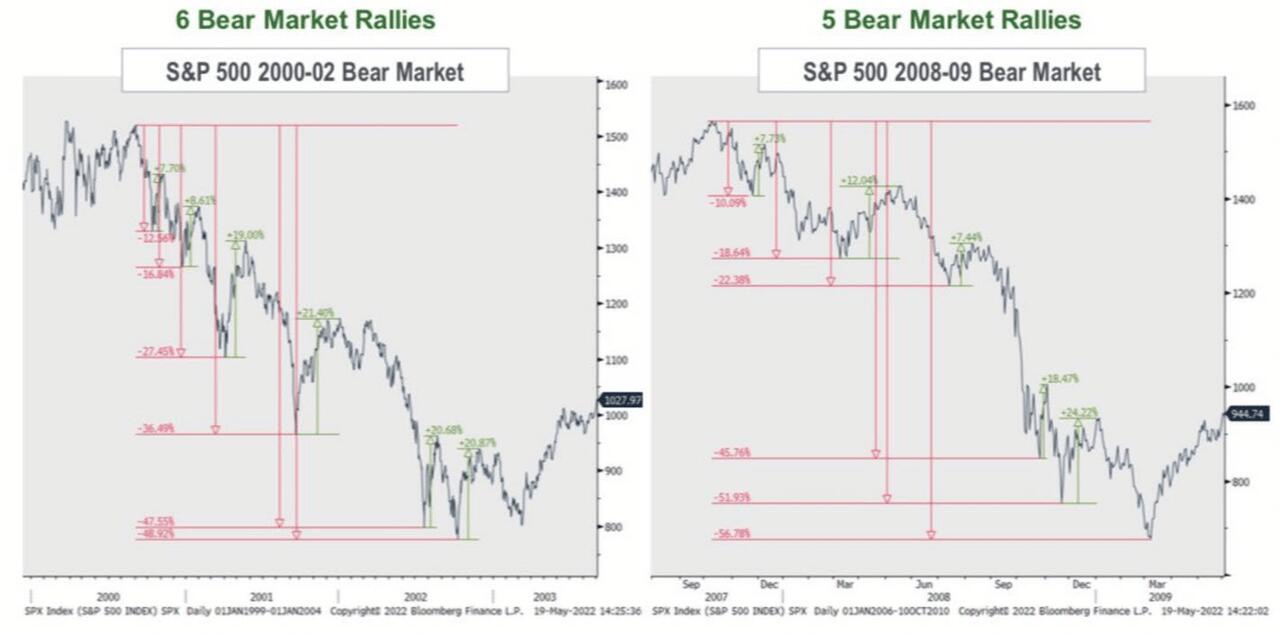

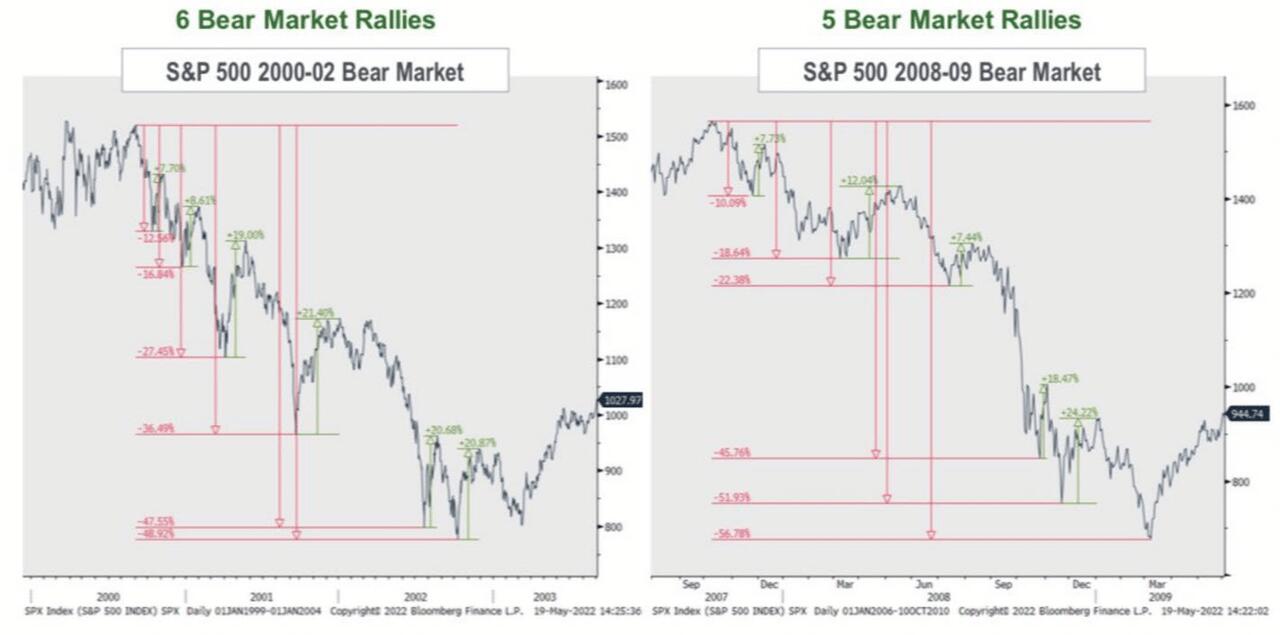

As shown below, the S&P 500 rallied nearly 15% for a month following the collapse of a significant 85-year-old investment bank. While the market didn’t regain its October 2007peak, animal spirits were rekindled for a brief while.

Investors looked the other way. They assumed whatever killed Bear Stearns was resolved. Despite improving investor sentiment, underlying fundamental conditions continued to worsen. Wall Street’s largest banks took advantage of the short-lived market stability to unload their riskiest positions on unsuspecting investors.

Telling the tale of the Bear Stearns rally and investors’ myopic vision in the spring of 2008 is a valuable lesson for today.

Bear Stearns

The failure of Bear Stearns was not a shock to most investors. In fact, many banks and a few notable hedge funds met a similar demise in the preceding two years. Further, house prices were falling, subprime loans were defaulting, CDOs were breaking, and a housing bubble of massive proportions was popping.

Low mortgage rates, relaxed borrowing standards, and poor banking regulation led to a housing bubble. Newly invented exotic financial derivatives tied to subprime mortgages multiplied the financial hardship for investors. We highly recommend reading or watching The Big Short by Michael Lewis for more information on the housing bubble.

The pin was nearing the bubble when Bear Stearns failed. Despite the proximity to a system-wide failure, investors ignored the writing on the wall. After a brief respite and a double-digit rally, new financial leaks started springing.

By late summer, it was apparent that Fannie Mae, Freddie Mac, AIG, and Countrywide were failing. Even the biggest banks and brokers like JP Morgan, Goldman Sachs, and Bank America were in trouble.

The post-Bear Stearns rally was an opportunity to sell stocks and reduce risks. Many investors paid dearly for ignoring the fundamentals and hoping the worst was behind them.

The Current Situation

In March 2020, the S&P 500 fell 30% in a matter of weeks as covid wreaked havoc on markets. With many facets of the economy primarily shuttered, the government became the economy. They flooded the economy with money, including the unprecedented step of writing checks directly to citizens and businesses.

The unemployment rate soared from 3.5% in February to 14.7% in April. But within months, the unemployment rate fell sharply. It ended December 2020 at 6.7% and now sits near 50-year lows.

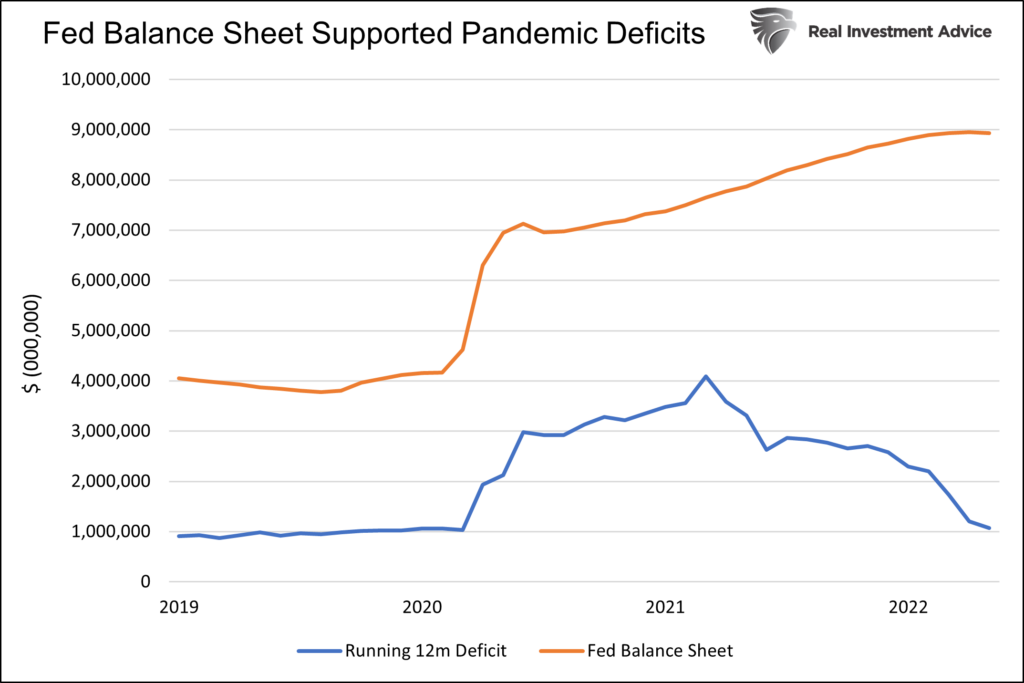

The Federal Reserve, via QE and very low-interest rates, was fully supportive of government deficits. In March 2020, the Fed lowered Fed Funds from 1.50% to 0%. Further, they embarked on a $120 billion a month bond-buying spree (QE). By December 31, 2021, the government deficit had grown by over $6 trillion. The Feds balance sheet nearly matched the increase. Despite a full economic recovery occurring much earlier in 2021, the government and Fed kept the fiscal and monetary gas pedals floored.

Investors quickly overcame their fear of covid. They were enamored by the monetary magic of the Fed and the direct and indirect liquidity it supplies markets. Investors didn’t fight the Fed. They embraced the government’s actions and bought relentlessly.

Don’t Fight the Fed

Since 2008, Fed liquidity via lower rates and QE has correlated well with increasing asset prices and valuations. Similarly, lower asset prices occurred in the brief instances where the Fed raised rates and did QT.

Valuations and fundamentals take a back seat to Fed monetary policy. From 2020 through 2021, valuations rose to record levels. Meme stocks and SPACs, many of which had little fundamental rationale, rose to crazy levels. High-growth technology stocks zoomed ahead.

Simply, the Fed, via substantial monetary easing, spurred speculative fever. While the Fed is not directly trafficking cash flows to markets, their actions are certainly abetting the behavior.

Is Another Bear Stearns Rally Happening?

Thus far, in 2022, the markets are trading poorly. The Fed is removing liquidity, and the government is sharply reducing spending. At the same time, the prior stimulus and covid-related supply line problems are pushing inflation to 40-year highs. The economy is slowing rapidly. For more recent evidence about weaker growth, check out our recent article, Snap Goes The Economy.

Fundamentally, the economic outlook is poor. Consumers are suffering and wages are not keeping up with inflation. Credit card spending has ramped up sharply to fill the gaps. Mortgage refinancing, a source of consumer dollars, is out of the question as mortgage rates surpass 5%.

Given high inflation, it remains unlikely the Fed will be able to juice markets as they might have in the past. Further, the coming elections and political dynamics make the passage of a fiscal spending bill very difficult.

Despite weakening economic data, the Fed claims tackling inflation is its number one goal. Now is not the time to fight the Fed. Nor is it the time to ignore fundamentals.

Unless the Fed pivots, inflation falls sharply, or financial instability occurs, take advantage of any Bear Stearns-like relief rallies. They provide opportunities to reduce exposure and rebalance your portfolio to a more conservative posture.

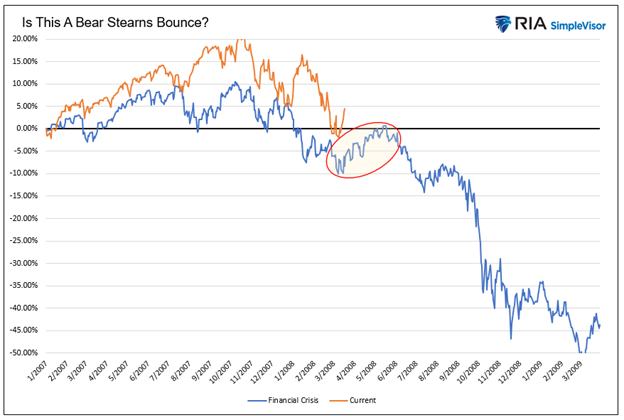

The graph below compares the 2008 bear market to the current decline. Might the recent uptick in asset prices be the 2022 version of the Bear Stearns bounce?

Summary

Do not let a market bounce blind you to the underlying fundamental, fiscal, and monetary conditions. Rising and falling markets are always accompanied by periods of counter-trend movement.

In bear markets, relief rallies are opportunities to rebalance and manage risk.

Authored by Michael Lebowitz via RealInvestementAdvice.com,

On Sunday, March 16, 2008, Bear Stearns was bought by JPM, with support and financial guarantees from the Fed, for $2 a share. It was quite the fall from $170 a year earlier.

Wall Street was in the early rounds of a bout with unprecedented financial instability, and the economy would soon follow. Investors were relieved Bear Stearns avoided bankruptcy in spite of the ominous clouds on the horizon and recent financial instability. Within hours of the market opening following the Bear Stearns takeover, stocks started rising and didn’t look back for a month.

As shown below, the S&P 500 rallied nearly 15% for a month following the collapse of a significant 85-year-old investment bank. While the market didn’t regain its October 2007peak, animal spirits were rekindled for a brief while.

Investors looked the other way. They assumed whatever killed Bear Stearns was resolved. Despite improving investor sentiment, underlying fundamental conditions continued to worsen. Wall Street’s largest banks took advantage of the short-lived market stability to unload their riskiest positions on unsuspecting investors.

Telling the tale of the Bear Stearns rally and investors’ myopic vision in the spring of 2008 is a valuable lesson for today.

Bear Stearns

The failure of Bear Stearns was not a shock to most investors. In fact, many banks and a few notable hedge funds met a similar demise in the preceding two years. Further, house prices were falling, subprime loans were defaulting, CDOs were breaking, and a housing bubble of massive proportions was popping.

Low mortgage rates, relaxed borrowing standards, and poor banking regulation led to a housing bubble. Newly invented exotic financial derivatives tied to subprime mortgages multiplied the financial hardship for investors. We highly recommend reading or watching The Big Short by Michael Lewis for more information on the housing bubble.

The pin was nearing the bubble when Bear Stearns failed. Despite the proximity to a system-wide failure, investors ignored the writing on the wall. After a brief respite and a double-digit rally, new financial leaks started springing.

By late summer, it was apparent that Fannie Mae, Freddie Mac, AIG, and Countrywide were failing. Even the biggest banks and brokers like JP Morgan, Goldman Sachs, and Bank America were in trouble.

The post-Bear Stearns rally was an opportunity to sell stocks and reduce risks. Many investors paid dearly for ignoring the fundamentals and hoping the worst was behind them.

The Current Situation

In March 2020, the S&P 500 fell 30% in a matter of weeks as covid wreaked havoc on markets. With many facets of the economy primarily shuttered, the government became the economy. They flooded the economy with money, including the unprecedented step of writing checks directly to citizens and businesses.

The unemployment rate soared from 3.5% in February to 14.7% in April. But within months, the unemployment rate fell sharply. It ended December 2020 at 6.7% and now sits near 50-year lows.

The Federal Reserve, via QE and very low-interest rates, was fully supportive of government deficits. In March 2020, the Fed lowered Fed Funds from 1.50% to 0%. Further, they embarked on a $120 billion a month bond-buying spree (QE). By December 31, 2021, the government deficit had grown by over $6 trillion. The Feds balance sheet nearly matched the increase. Despite a full economic recovery occurring much earlier in 2021, the government and Fed kept the fiscal and monetary gas pedals floored.

Investors quickly overcame their fear of covid. They were enamored by the monetary magic of the Fed and the direct and indirect liquidity it supplies markets. Investors didn’t fight the Fed. They embraced the government’s actions and bought relentlessly.

Don’t Fight the Fed

Since 2008, Fed liquidity via lower rates and QE has correlated well with increasing asset prices and valuations. Similarly, lower asset prices occurred in the brief instances where the Fed raised rates and did QT.

Valuations and fundamentals take a back seat to Fed monetary policy. From 2020 through 2021, valuations rose to record levels. Meme stocks and SPACs, many of which had little fundamental rationale, rose to crazy levels. High-growth technology stocks zoomed ahead.

Simply, the Fed, via substantial monetary easing, spurred speculative fever. While the Fed is not directly trafficking cash flows to markets, their actions are certainly abetting the behavior.

Is Another Bear Stearns Rally Happening?

Thus far, in 2022, the markets are trading poorly. The Fed is removing liquidity, and the government is sharply reducing spending. At the same time, the prior stimulus and covid-related supply line problems are pushing inflation to 40-year highs. The economy is slowing rapidly. For more recent evidence about weaker growth, check out our recent article, Snap Goes The Economy.

Fundamentally, the economic outlook is poor. Consumers are suffering and wages are not keeping up with inflation. Credit card spending has ramped up sharply to fill the gaps. Mortgage refinancing, a source of consumer dollars, is out of the question as mortgage rates surpass 5%.

Given high inflation, it remains unlikely the Fed will be able to juice markets as they might have in the past. Further, the coming elections and political dynamics make the passage of a fiscal spending bill very difficult.

Despite weakening economic data, the Fed claims tackling inflation is its number one goal. Now is not the time to fight the Fed. Nor is it the time to ignore fundamentals.

Unless the Fed pivots, inflation falls sharply, or financial instability occurs, take advantage of any Bear Stearns-like relief rallies. They provide opportunities to reduce exposure and rebalance your portfolio to a more conservative posture.

The graph below compares the 2008 bear market to the current decline. Might the recent uptick in asset prices be the 2022 version of the Bear Stearns bounce?

Summary

Do not let a market bounce blind you to the underlying fundamental, fiscal, and monetary conditions. Rising and falling markets are always accompanied by periods of counter-trend movement.

In bear markets, relief rallies are opportunities to rebalance and manage risk.